With an abundance of natural resources across land and sea, Australia is well equipped for a diverse, renewable energy system. In fact, it has the world’s highest solar radiation per square metre so it’s hardly surprising that 1 in 3 households now have rooftop solar PV. The hard work, though, comes in weaning its grid off fossil fuels that still contribute to a total of 71% of electricity generated every year, of which coal provides 51%. Energy storage will play a mammoth role in enabling the country to achieve net zero by 2050 and that’s why the government’s first National Electric Vehicle Strategy launched a few weeks ago has been so highly anticipated.

While Australia has a number of large, industrial grid batteries providing 7.8GW of storage, the flexible capacity created through millions of electric vehicles (EVs) is attracting more attention from policy makers, grid operators and auto OEMs alike.

The new strategy looks at a wide range of topics associated with EVs from a ‘Fuel Efficiency Standard’ implementation to creating a plan for charging infrastructure, but I believe the most important driving force of the paper is for better customer incentives to switch to an EV and allow Australia to start catching up with its international peers. Some could even argue that Australia’s relatively slow progress on EV adoption to date (according to the new strategy, EV market share is one fifth of that compared to many European countries) means it is now uniquely positioned to leverage learnings across customer behaviour, technology and policies from markets that are further ahead.

Is the grass greener on the other side?

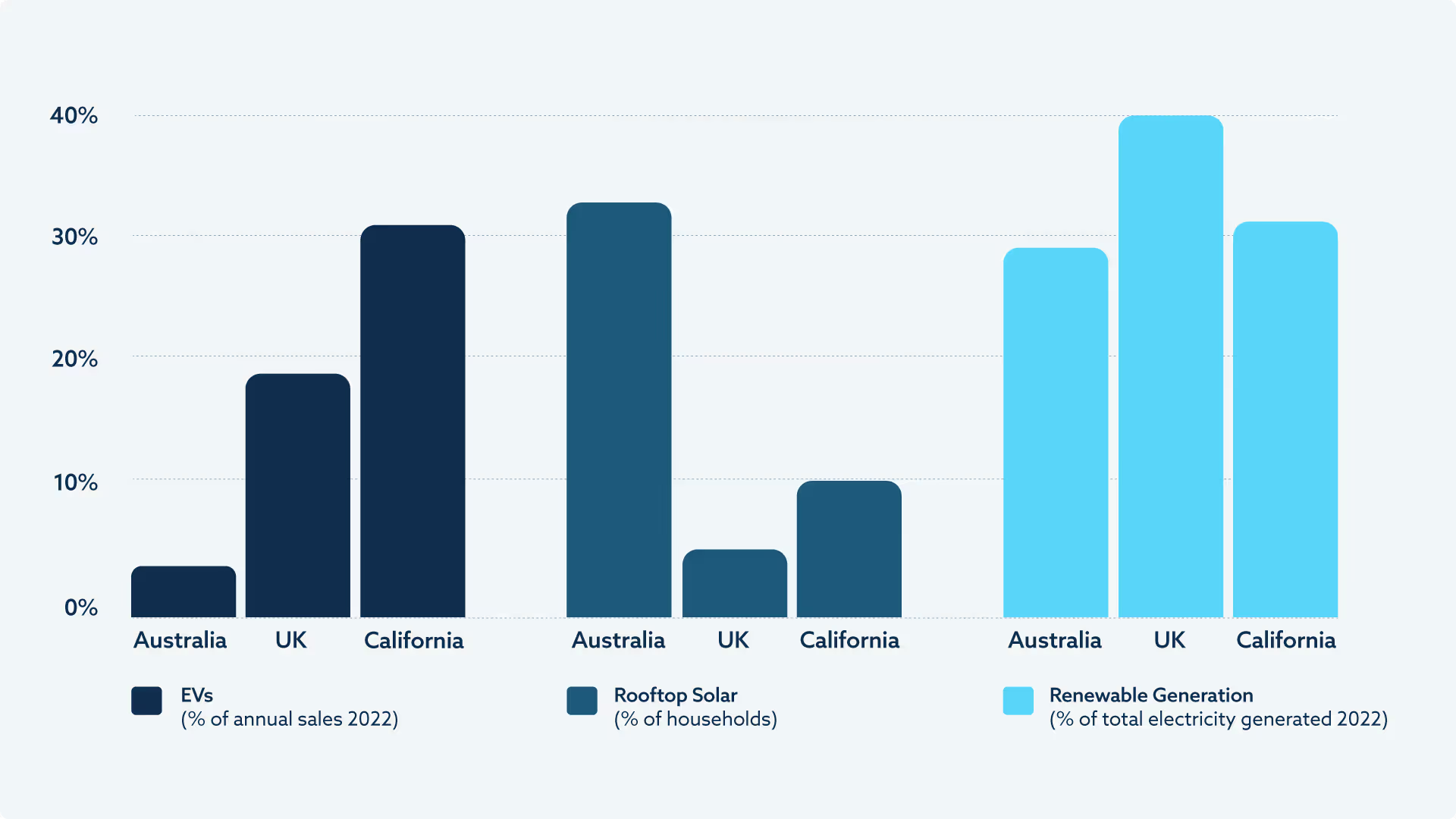

Both the UK and California are global leaders when it comes to electrifying transport. In 2022, EVs represented ~22% of vehicles sold across the UK and 16% of vehicles sold across California. So what is the impact on their respective energy markets?

Our own data from more than 12,000 EV drivers shows that, in the UK, EVs represent a ~75% increase in household electricity consumption. This, paired with the ambition to reach net zero by 2030 – when currently just over 40% of the nation’s power mix is renewable – is shaking up the energy market from generation to consumption and even bidirectional energy flow.

Meanwhile, California is facing its own set of unique challenges. Coined the ‘duck curve’, the electricity system operator is having to manage increasingly rapid afternoon demand spikes as the sun goes down and solar generation capacity drops, as well as manage increasingly common extreme weather events.

Regulators in California and the UK are responding by creating market mechanisms to drive relevant demand behaviours and to manage potential peak demand (DFS activities in the UK, ELRP and other DR markets in California) with electric vehicle flexibility front and centre.

Smart charging: More money in wallets, less CO2 in the air

So, what could smart charging mean for Australia? Assuming a scenario where all 15 million passenger vehicles on Australian roads are EVs, smart charging can deliver more than an 8GW reduction in the daily peak load and shift this load to times when renewables (from the grid or rooftops) are available. If technologies like V2X are adopted, EVs can represent a 18GW peak load reduction and further benefits to driving grid decarbonisation and cost savings.

So what can Australia learn from other markets? Here are some of the key things we have learned in four years through our international programmes:

1. Smart charging is make or break for successful EV adoption

Even in those markets where EV uptake is higher, the proportion of EV owners who are smart charging is comparatively low. For example, in the UK, research has shown only 27% of EV owners are using smart scheduling for their vehicle charging. And only a fraction of customers consider changing their energy supply contract to one that includes EV charging rewards. Clearly, customers simply aren’t aware that smart charging exists and what tariffs are available to them – if they did we would see far higher adoption rates because of how tangible and easy-to-access the benefits are.

Australia is well positioned to learn from other markets and bridge this gap in smart charging adoption early by creating a more seamless customer experience from ICE to EV that brings about the most value for customers and the energy system. This will take tight cross-industry collaboration, where energy suppliers build propositions that are easy-to-understand and accessible to all, and market regulators proactively recognise the value of EV smart charging for decarbonisation.

2. Auto OEMs can ease customers’ pain of moving to an EV

The volume of information facing an EV customer can be overwhelming and is largely due to the current complexity of the EV ecosystem and the number of different players involved at each stage of the journey. An average customer needs to interact with at least six different parties at various points of their journey in order to receive the ‘full EV experience’.

The good news is, much of a driver’s interaction with their EV is via their auto OEM’s app, so OEMs are well placed to influence key customer decision making around charging and other aspects of their experience. And it’s not all up to the OEM, energy suppliers need to build strong collaboration with OEMs and dealerships to make switching to smart charging products as easy as possible.

3. Grids need to gear up for domestic flexibility, fast

While creating a seamless and simple customer experience is vital, it’s no silver bullet. To unleash the full potential of EV’s storage potential we need the energy markets themselves to be set up in a way that will maximise the value of these distributed resources. Regulators and policymakers need to cultivate appropriate market structures and incentives and encourage smart meter deployment, introduce more dynamic pricing opportunities and facilitate ancillary markets that can be accessed by all technologies.

We have already seen that the lack of regulatory clarity and the slow pace of market development has considerable impact on customers being able to access the value from ‘smarter’ ways of consuming their energy. The longer it takes to create the right market conditions, the harder it becomes to engage EV customers in smart charging and other EV technologies that bolster decarbonisation and grid resilience.

4. New technologies are friends not foes

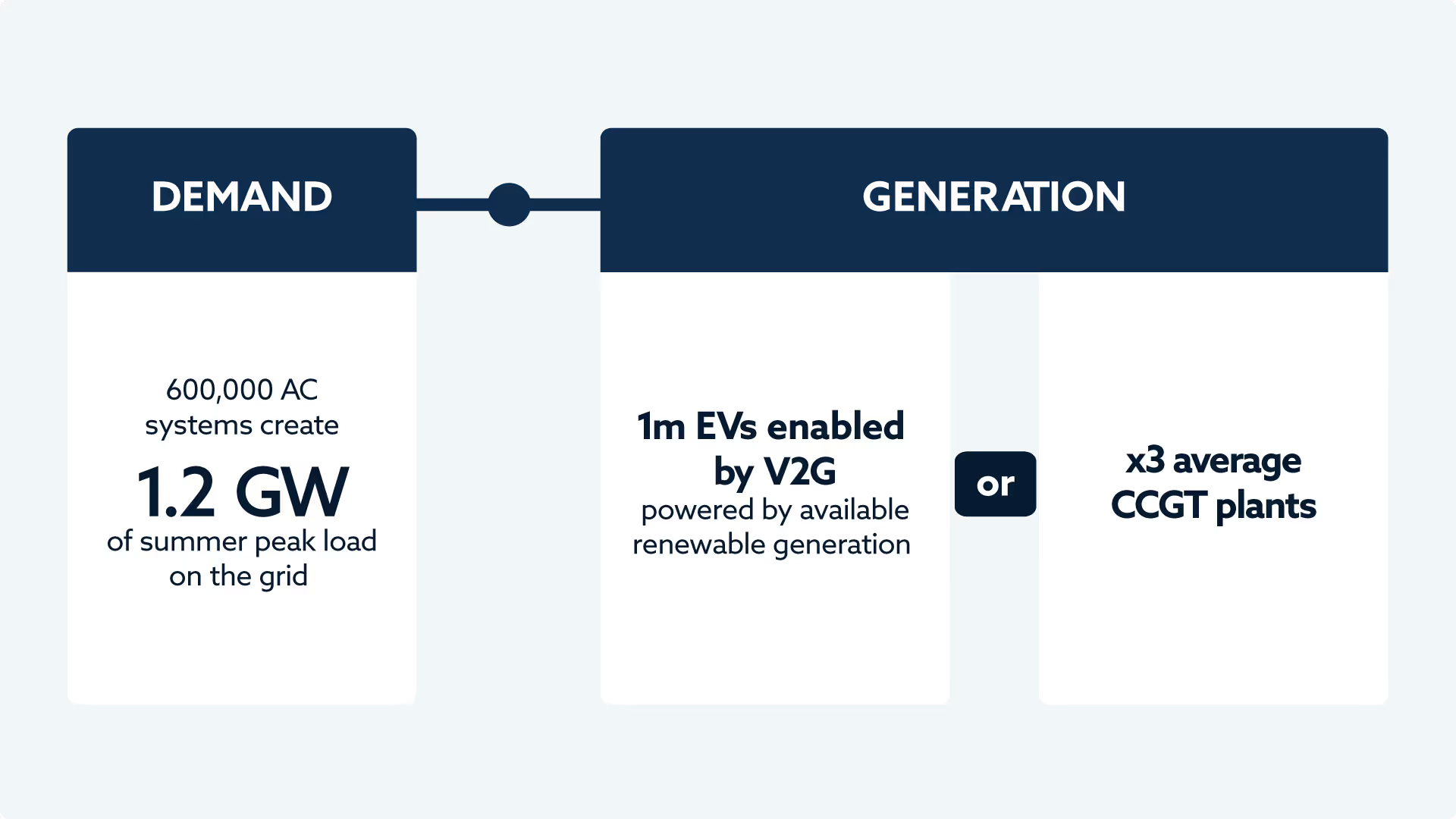

In the EV space, bi-directional charging can deliver exponential benefits to the EV drivers and electricity system. However, the deployment of this is highly dependent on all of the above points. If the right lessons are taken from markets like the UK (for more detail read our white paper: ‘What’s Next for V2X?’) significant benefits can be unlocked. As shown in the example below, 1 million V2X-enabled EVs represent 1.2GW of flexible daily load and can play a direct role in displacing 3 average CCGT power plants with renewables like wind and solar.

Work is underway: Kaluza x AGL Energy

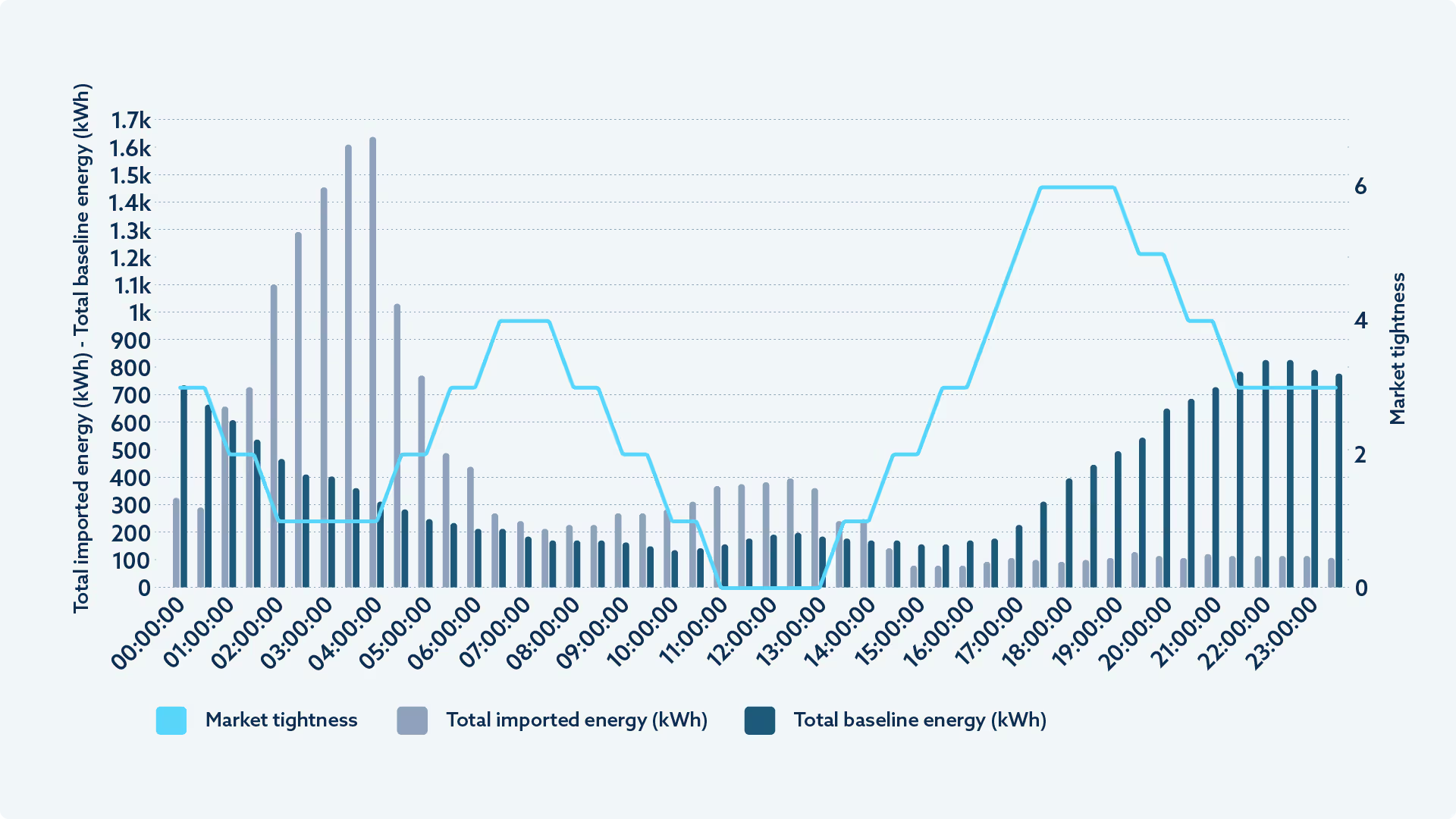

Kaluza has already started laying the foundations for cost-effective EV charging in collaboration with AGL Energy, one of Australia’s leading energy service providers. Last year, we launched a managed charging program that has resulted in 98% of the participating EV charging being shifted to off-peak times and unlocking up to AU$20 savings per month. By creating easy and rewarding charging experiences, AGL Energy is accelerating the adoption of EVs in Australia, boosting customer engagement and driving decarbonisation.

See below a snapshot of how we optimised the importing of energy into the connected EVs as demand on the grid ‘market tightness’ fluctuated throughout the day.

And this is just the beginning. We look forward to how the new EV strategy will invigorate more progress across suppliers, OEMs, grid operators and technology partners to put Australia firmly on its path to net zero.

*’Electric Vehicle Smart Chargepoint Survey 2022‘, BEIS, 2022